Americans face a choice between credit card (debt consolidation vs balance transfer) debt consolidation and balance transfer options as nearly 83% of them make debt repayment their priority this year. The average American carries almost $8,000 in credit card debt, making economical solutions crucial right now. The situation looks even more pressing since almost 53% of Americans pay over half their monthly income just for housing, which leaves them with less money for other expenses and pushes them toward more credit card debt.

Balance transfers look attractive with their zero interest for up to 21 months, while debt consolidation loans come with fixed interest rates between 10-15% – substantially lower than regular credit card rates that exceed 20%. The math tells an interesting story. Take someone with $10,000 in credit card debt at 22% APR. They would pay about $3,748 in interest over three years. A personal loan at 13% APR would cost just $2,129 in interest, saving them over $1,600. But there’s a catch. Balance transfer fees usually run 3-5%, and many people who unite their debt end up with credit card balances back at pre-consolidation levels within 18 months. The real question becomes: which choice will save you more money in 2025?

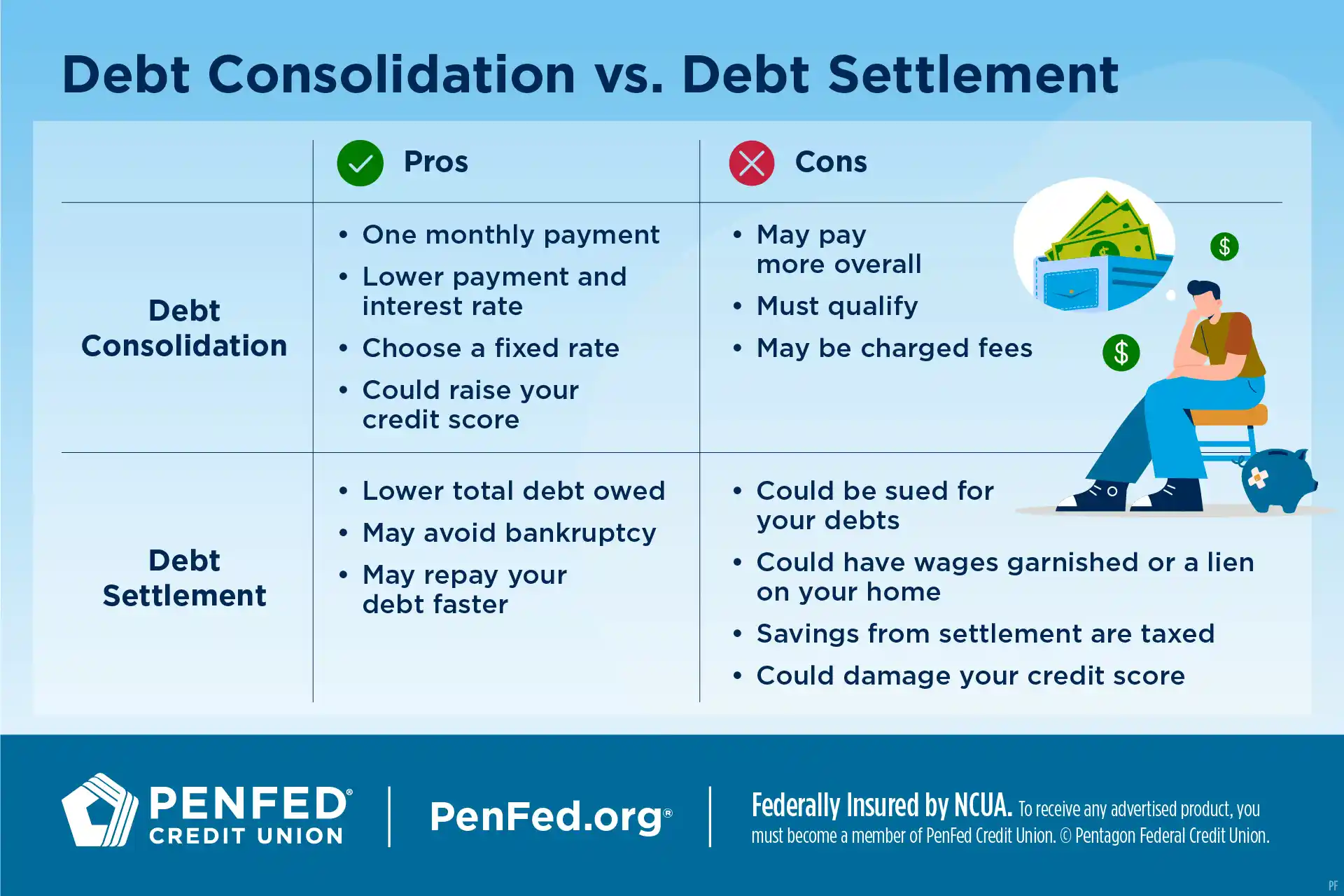

Understanding the Basics: Balance Transfer vs Debt Consolidation

Image Source: PenFed Credit Union

Let’s look at the basic differences between two popular ways to handle debt. People who need to deal with high-interest credit card debt often look at balance transfers or debt consolidation loans as ways to get out of debt.

What is a balance transfer and how does it work?

A balance transfer moves your outstanding debt from one or more credit cards to another card that usually comes with a lower promotional interest rate. Credit card companies offer introductory 0% APR periods that last between 6 and 21 months. You won’t pay any interest on transferred balances during this time, which means every dollar you pay reduces your actual debt.

You’ll need to complete the transfer quickly, usually within two months after opening the new account. Most cards charge a fee of 3% to 5% of the amount you transfer. To cite an instance, if you move $5,000 from a card with 15% APR to one with 0% promotional APR, you could save about $265 in interest, even after paying the transfer fees.

How debt consolidation loans simplify repayment

Debt consolidation loans give you a lump sum of money to pay off multiple unsecured debts at once. Once you’ve paid off existing debts, you make one fixed monthly payment on the new loan. These loans usually need to be paid back in one to seven years.

Most debt consolidation loans are unsecured personal loans with fixed interest rates from 6% to 36%, based on your credit score. Lenders might charge origination fees between 1% and 10% of what you borrow. You can typically borrow anywhere from $1,000 to $50,000, and some lenders offer up to $100,000.

Key differences between revolving and installment credit

The main difference between these options comes down to their credit structure. Balance transfers use revolving credit, which lets you repeatedly use and pay back money up to your credit limit. Credit cards show how revolving credit works—you can pay different amounts each month based on what you owe.

Debt consolidation loans work differently as installment credit, giving you one lump sum with set repayment terms. Unlike revolving accounts, your monthly payments stay the same until you’ve paid off the loan.

Your credit utilization affects your credit scores a lot, but this mainly applies to revolving accounts. Missing payments on either type of credit hurts your score, but how you handle revolving credit tends to matter more because it shows how well you manage changing expenses and plan your finances.

Cost Comparison: Which Option Saves More in 2025?

Image Source: Verified Market Research

The numbers tell a clear story about how these two options affect your finances. Let’s look at the specific costs to help you save more money in 2025.

Interest savings: 0% APR vs fixed loan rates

These options have very different interest structures. Balance transfer cards come with 0% introductory APRs that last 12 to 18 months. Your payments during this time directly reduce your debt. The rates jump substantially after the promotional period ends and can go above 20%.

Debt consolidation loans work differently. They have fixed rates between 6% and 36%, based on your credit score. People with excellent credit might get rates under 7%. Right now, the average personal loan rate sits at 12.46%. This is a big deal as it means that someone with $10,000 in credit card debt at 22% APR would pay $3,748 in interest over three years. The same person would pay just $2,129 with a personal loan at 13% APR—putting $1,600 back in their pocket.

Balance transfer fees vs loan origination fees

Balance transfer cards usually take 3% to 5% of the transferred amount as fees. Moving $10,000 costs you $300 to $500 right away.

Loan origination fees range from 1% to 10% of the borrowed amount. People with good credit scores often pay less than balance transfer fees. Some lenders even skip these fees entirely.

Monthly payment comparison: short-term vs long-term

Balance transfers give you flexible monthly minimums but need discipline to clear the debt before promotional rates end. Consolidation loans provide predictable monthly payments that stay the same until you pay off the loan.

Remember this: consolidation loans don’t let you make minimum payments. This might not work well if your income changes month to month.

Total repayment cost: 18 months vs 5 years

Balance transfers save you more money in shorter timeframes, especially if you pay everything during the 0% period. For 5-year repayment plans, consolidation loans often work out cheaper overall, even though interest starts immediately.

Your credit score makes a huge difference. Excellent credit (720-850) gets you personal loan rates around 13.88%. Fair credit (630-689) pushes those rates up to about 19.77%.

When Each Option Makes the Most Sense

Your financial situation determines whether debt consolidation or balance transfer makes more sense. Each option works better in different cases based on your timeline, debt amount, and credit profile.

Best for short-term payoff: Balance transfer scenarios

Balance transfer cards work great if you can pay off debt within a set timeframe. You’ll get the most value by paying the entire balance during the intro period, which usually lasts 15-21 months. These cards are a perfect fit for smaller debt amounts that you can eliminate before the promotional rate ends. People with excellent credit and enough income to make bigger monthly payments will see the best results. Let’s say you have $15,000 in credit card debt at 22% APR – moving it to a 0% card would mean monthly payments of about $861 to clear everything within an 18-month promotional period.

Best for long-term budgeting: Debt consolidation use cases

Debt consolidation loans give you structure with fixed payments over longer periods. These loans make sense if you need one to seven years to clear larger debt amounts. Many people like consolidation loans because their payments stay the same month after month. On top of that, they help if you want longer repayment terms with lower monthly payments—about $297 monthly for a $15,000 debt over five years at 7% interest.

How credit score affects your eligibility and savings

Credit scores have a big effect on your options. Balance transfers usually need good to excellent credit scores (690+), and the average approved score is 727. Debt consolidation loans are available to people with various credit scores, including fair credit. Your credit score directly relates to interest rates—excellent credit might get you rates under 7%, while fair credit could mean rates close to 20%.

Discover card debt consolidation loans vs Citi balance transfer card

Discover personal loans focus on debt consolidation and come with no annual fees. Meanwhile, Citi Simplicity Card gives you one of the longest intro periods for balance transfers without late fees. Your payoff timeline should guide your choice between these options rather than brand preference.

Risks, Credit Impact, and Long-Term Considerations

Image Source: LoansJagat.com

Money matters go beyond the here and now when you look at debt consolidation and balance transfer options. You need to know these risks to make better choices about your financial future.

How each option affects your credit score

A hard inquiry happens when you apply for a balance transfer card or consolidation loan. This usually takes less than five points off your credit score. The long-term impact looks quite different though. Your credit can improve with debt consolidation loans. These loans lower your utilization ratio and create a better credit mix. Balance transfers might boost your score if you keep your old accounts open. However, new cards can hurt your credit over time if you open too many.

Risk of accumulating new debt after consolidation

A 2023 TransUnion survey revealed something worrying. People who took personal loans to unite their debts saw their credit card balances bounce back to previous levels in just 18 months. This shows a big problem: moving debt around won’t fix it unless you change how you spend money.

What happens if you miss payments?

Late payments create a domino effect of problems. Your score can drop by 110 points with just one missed payment. Most creditors will double your normal rate after 60 days – they call this penalty APR. Your account moves to collections after six months without payment. This black mark stays on your credit report for seven years.

Behavioral traps: Spending habits post-consolidation

The biggest problem comes from seeing consolidation as the answer instead of a tool. Many people clear their credit cards through consolidation and feel relieved. Then they rack up new balances. You might end up in worse shape than before if you don’t stick to a realistic budget. You could have both consolidation payments and fresh credit card debt. Good debt management needs more than restructuring – it demands a complete change in how you handle money.

Comparison Table

|

Feature |

Balance Transfer |

Debt Consolidation Loans |

|---|---|---|

|

Interest Rates |

0% APR for 12-21 months (promotional), 20%+ after promotion ends |

6-36% fixed APR (average 12.46%) |

|

Typical Fees |

3-5% transfer fee |

1-10% origination fee |

|

Payment Structure |

Variable monthly minimums |

Fixed monthly payments |

|

Typical Term Length |

12-21 months (promotional period) |

1-7 years |

|

Credit Score Requirements |

Good to excellent (690+), average approval score 727 |

Available to borrowers of all credit levels, including fair credit |

|

Loan/Transfer Amounts |

Not specifically mentioned |

$1,000 to $50,000 (up to $100,000 with select lenders) |

|

Best Suited For |

Short-term payoff, smaller debt amounts |

Long-term budgeting, larger debt amounts |

|

Credit Impact |

Credit score dips briefly from hard inquiry, score can improve when old accounts remain open |

Brief score decrease from hard inquiry, potential improvement in utilization ratio and credit mix |

|

Risk Factors |

High interest rates take effect after promotional period |

Credit card balances might return to pre-consolidation levels within 18 months |

|

Example Savings |

$265 on $5,000 transfer (after fees) |

$1,600 on $10,000 over 3 years (13% APR vs 22% credit card APR) |

Conclusion

Your specific financial situation and debt repayment timeline will determine whether you should choose debt consolidation loans or balance transfers. Both options can help you get relief from high-interest credit card debt in 2025.

Balance transfers work best if you have smaller debt amounts and can pay off your balances within the promotional period. You might save a lot of money with this approach, especially with promotional periods that last up to 21 months. The zero interest during this time lets you tackle your principal debt head-on.

Debt consolidation loans give you a more structured path when you have larger debt loads or need more time to repay. These loans come with predictable fixed monthly payments and often have lower interest rates than standard credit cards. People who need several years to clear their debt usually do better with consolidation loans, even though interest starts right away.

Your credit score plays a big role in what options you can get. People with scores above 690 usually qualify for the best offers for both options. Those with fair credit might find it easier to get consolidation loans than premium balance transfer cards.

Final Thoughts:

Both strategies come with their risks. Credit card balances often return to pre-consolidation levels within 18 months. This shows that you need to change your spending habits – debt restructuring alone won’t fix the problem. Real financial success comes from changing your behavior while restructuring your debt.

Missing payments can hurt badly. Your credit score could drop by 110 points or more after just one late payment. That’s why you need to pick an option that fits your budget.

The math favors balance transfers for short-term payoff and consolidation loans for longer-term plans. Let’s say you have $10,000 in credit card debt at 22% APR. You could save over $1,600 by using a consolidation loan at 13% APR instead of making minimum payments on the original card.

Take time to look at your debt amount, repayment timeline, credit profile, and spending habits before you decide. The best approach combines debt restructuring with real changes to your budget to keep debt from piling up again. A good debt management strategy needs to handle both your current financial pressure and your long-term financial health.

FAQ

Q1. Which option is better for short-term debt repayment: balance transfer or debt consolidation?

Balance transfers are generally better for short-term debt repayment, especially if you can pay off the entire balance during the promotional period (typically 12-21 months). They work best for smaller debt amounts and for individuals with excellent credit who can make aggressive monthly payments.

Q2. How does credit score affect eligibility for balance transfers and debt consolidation loans?

Credit scores significantly impact eligibility and terms. Balance transfers typically require good to excellent credit scores (690+), with an average approved score of 727. Debt consolidation loans are more accessible across the credit spectrum, including for those with fair credit, but interest rates correlate directly with credit scores.

Q3. What are the risks of accumulating new debt after consolidation?

A major risk is accumulating new debt after consolidation. Studies show that many consumers see their credit card balances return to pre-consolidation levels within 18 months. Without addressing underlying spending habits, consolidation may simply shuffle debt rather than eliminate it.

Q4. How do balance transfers and debt consolidation loans affect credit scores?

Initially, both options may cause a temporary credit score dip due to hard inquiries. Long-term, debt consolidation loans can improve your credit by lowering your utilization ratio and diversifying your credit mix. Balance transfers may improve your score if you keep old accounts open, but repeatedly opening new cards can damage your credit over time.

Q5. What happens if you miss payments on a balance transfer or debt consolidation loan?

Missing payments on either option can have severe consequences. A single missed payment can drop your credit score by up to 110 points. After 60 days, most creditors apply penalty APRs, often doubling your normal rate. After six months of nonpayment, accounts typically enter charge-off status and move to collections, remaining on your credit report for seven years.

You might also like: How to Get a Loan with Bad Credit in 2025: A Simple Step-by-Step Guide

References

[1] – https://www.cbsnews.com/news/balance-transfer-or-debt-consolidation-better-right-now-experts-weigh-in/

[2] – https://www.cnbc.com/select/debt-consolidation-pros-cons/

[3] – https://www.citi.com/personal-loans/learning-center/basics/balance-transfer-vs-personal-loan

[4] – https://www.consolidatedcredit.org/financial-news/effects-of-missed-payments/

[5] – https://www.nerdwallet.com/article/loans/personal-loans/debt-consolidation-credit-card-balance-transfer

[6] – https://www.experian.com/blogs/ask-experian/revolving-vs-installment-credit/

[7] – https://www.investopedia.com/ask/answers/110614/what-are-differences-between-revolving-credit-and-installment-credit.asp

[8] – https://www.cnbc.com/select/which-should-you-have-revolving-credit-or-installment-credit/

[9] – https://www.bankrate.com/loans/personal-loans/balance-transfer-credit-card-vs-personal-loan/

[10] – https://blog.harvardfcu.org/debt-consolidation-loan-or-balance-transfer-know-your-options

[11] – https://www.cnbc.com/select/how-to-choose-between-loan-and-zero-percent-apr-card-for-debt/

[12] – https://www.nerdwallet.com/calculator/personal-loan-calculator

[13] – https://www.nerdwallet.com/best/credit-cards/balance-transfer

[14] – https://www.experian.com/blogs/ask-experian/pros-and-cons-of-debt-consolidation/

[15] – https://www.iwillteachyoutoberich.com/pros-and-cons-of-debt-consolidation/

[16] – https://www.equifax.com/personal/education/credit-cards/articles/-/learn/balance-transfers-impact-credit-score/

[17] – https://www.greenpath.com/blog/debt/debt-consolidation-loan-or-balance-transfer/

[18] – https://www.creditninja.com/faq/what-happens-if-you-dont-pay-debt-consolidation-loans/

By

By

By

By

By

By